Umbrella Insurance in 2026: The Quiet Shield Protecting High-Net-Worth Families

If you’ve spent years building serious wealth—real estate, investments, business equity—you probably assume your insurance coverage is already strong. After all, your home and auto policies likely carry higher limits than average.

Here’s the uncomfortable truth: those policies usually stop working long before the real financial damage begins.

That’s where umbrella insurance comes in.

Think of it as a second layer of protection. Your homeowners, auto, or boat policy handles the first wave of liability. When those limits run out, the umbrella policy steps in and absorbs the remaining cost. Without that extra layer, the difference comes straight out of your assets.

And in 2026, that difference can be massive.

Why Wealth Makes You a Bigger Legal Target

Success attracts attention. Unfortunately, not all of it is positive.

In legal circles, wealthy defendants are often referred to as “deep pockets.” Plaintiff attorneys know that cases involving affluent individuals are more likely to produce large settlements. That reality shapes how lawsuits are filed and how aggressively they’re pursued.

What’s changed recently is how easy it is to estimate someone’s wealth.

Public records, property databases, social media, and corporate filings reveal far more than most people realize. A lawyer preparing a case can quickly piece together a rough picture of your financial standing before the first hearing even begins.

Own property in a prestigious ZIP code?

Serve on a company board?

Post about travel, cars, or investments online?

All of those signals increase the likelihood that a lawsuit will demand higher damages.

And the risk isn’t necessarily tied to wrongdoing. Sometimes it’s simply about capacity to pay. A serious accident, a dispute involving employees, even a careless online comment—any of these can trigger litigation.

Without proper protection, a lawsuit can start dismantling a lifetime of financial planning in a matter of hours.

The Hidden Weakness in Standard Insurance

Many affluent households assume their existing policies are already “full coverage.” The term sounds reassuring.

But it’s misleading.

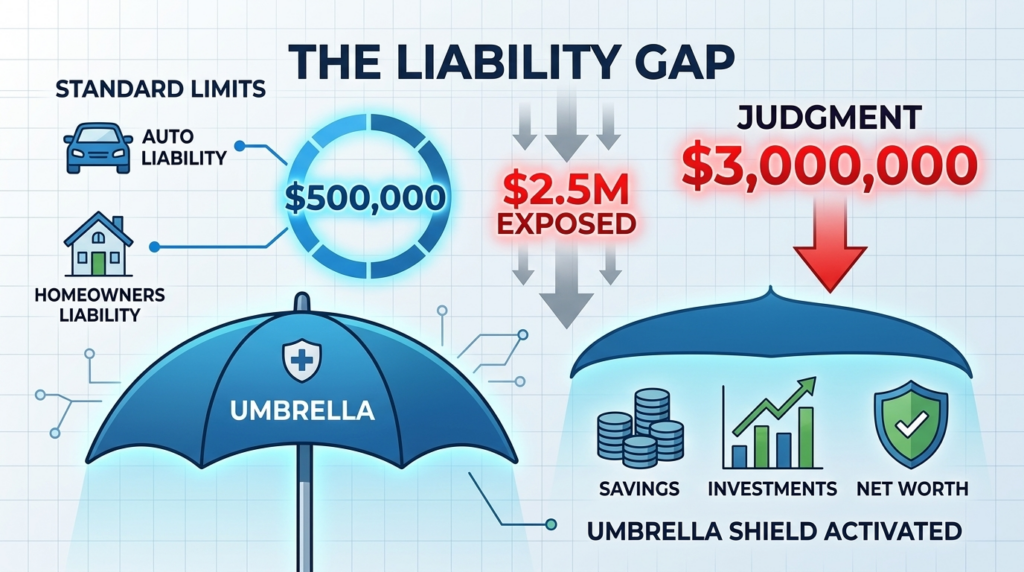

Most auto and homeowners policies carry liability limits that look like this:

- Auto liability: $250,000 to $500,000

- Homeowners liability: $300,000 to $500,000

Those numbers once felt generous. Today they’re barely adequate.

Medical inflation alone has pushed severe injury settlements dramatically higher. Add legal fees, lost wages, and emotional damages, and the total climbs fast.

By 2026, major injury cases frequently land in this range:

$2 million to $5 million — sometimes far more.

Large jury awards—often called “nuclear verdicts”—are also becoming more common. Juries increasingly deliver eight-figure outcomes in catastrophic injury cases.

Now imagine the math.

If your policy covers $500,000 and the court awards $3 million, that leaves $2.5 million exposed. Without umbrella insurance, the court can pursue your personal assets to satisfy the judgment.

Savings. Brokerage accounts. Even future earnings.

That’s the gap umbrella insurance was designed to close.

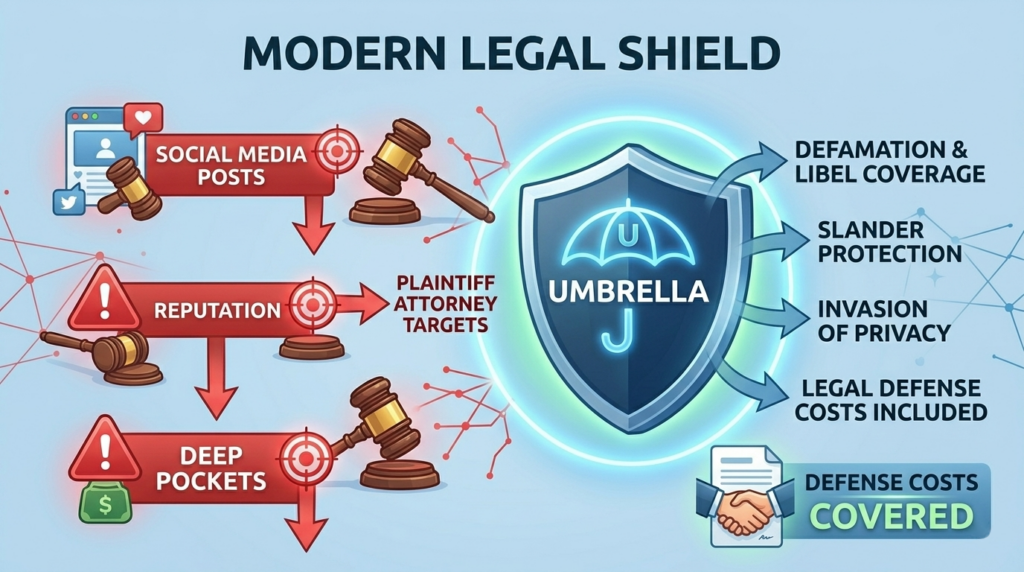

The Social Media Liability Most People Ignore

Physical accidents aren’t the only threat anymore.

One of the most valuable features in modern umbrella policies is protection against personal injury claims—legal language that covers non-physical harm.

That includes:

- Libel

- Slander

- Defamation

- Invasion of privacy

These risks have exploded in the social media era.

A single post, review, or comment can trigger a lawsuit if someone believes their reputation was harmed. Even if the claim ultimately fails, the legal defense costs can spiral into six figures long before the case reaches trial.

Standard homeowners policies often exclude or limit these claims. Many people don’t realize that gap exists until a lawyer points it out.

A well-structured umbrella policy typically expands protection to cover these modern risks—including the legal defense itself.

That protection alone can justify the policy.

How Much Umbrella Coverage Do You Actually Need?

Buying umbrella insurance isn’t just about picking a number that “sounds big.”

The real question is: how much of your wealth is exposed?

A common mistake is purchasing a basic $1 million umbrella policy and assuming it solves the problem. For many households, that’s just the starting point.

A more practical guideline looks something like this:

| Net Worth | Suggested Umbrella Coverage |

| $1M – $5M | $2M – $5M |

| $5M – $10M | $5M – $10M |

| $10M+ | $10M – $25M+ |

The logic is straightforward. Liability coverage should roughly match the amount of wealth that could realistically be targeted in a lawsuit.

For households earning over $200,000 annually, even a modest umbrella policy has become standard practice.

For high-net-worth families, higher limits are often essential.

Not All Insurance Carriers Handle High Net Worth Well

Another detail many people overlook: umbrella insurance isn’t identical across insurers.

When researching policies, look for carriers experienced with high-net-worth clients. These companies understand the complexities that come with larger financial lives.

That includes risks tied to:

- Multiple properties

- Domestic staff

- Vacation homes

- International travel

- Collectibles and luxury assets

Standard insurers sometimes struggle with these scenarios because their policies are built for mass-market customers.

Specialized carriers structure coverage differently and often offer significantly higher limits.

If your financial situation has grown more complex over the years, the right insurer matters just as much as the policy itself.

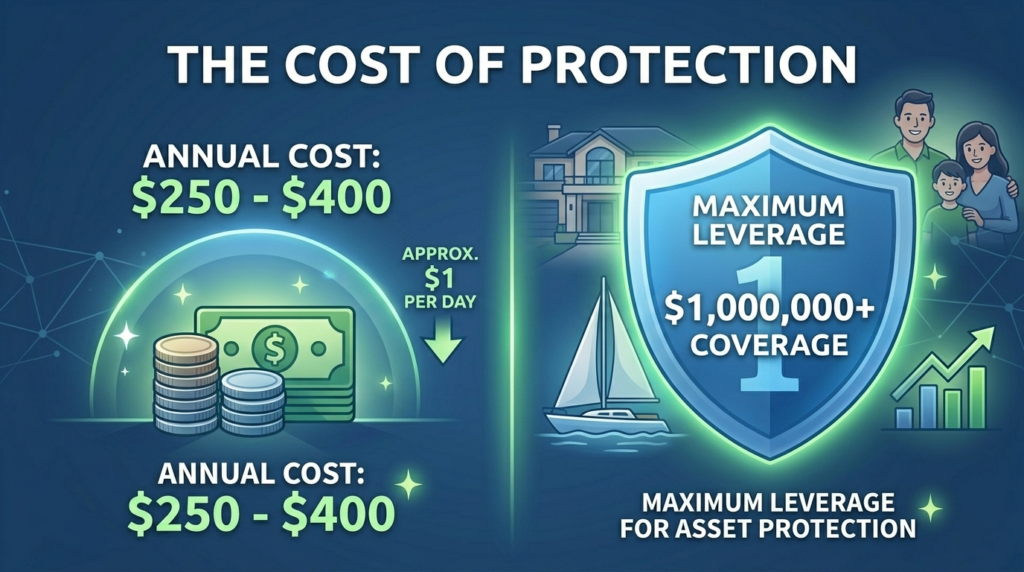

Why Umbrella Insurance Is Surprisingly Affordable

Here’s the surprising part.

Despite the enormous protection it provides, umbrella insurance is relatively inexpensive.

Because it only activates after underlying policies are exhausted, insurers treat it as secondary coverage. That dramatically lowers the price compared with primary liability insurance.

Typical annual costs in 2026 look like this:

- First $1 million of coverage: about $250–$400 per year

- Each additional $1 million: often $100–$200

That means a $5 million umbrella policy might cost roughly $600–$1,000 annually.

Put differently, the price of one upscale dinner in Manhattan or Los Angeles could fund an entire year of asset protection.

From a financial perspective, very few risk-management tools offer that kind of leverage.

The Smart Way to Add Umbrella Coverage

If you’re considering umbrella insurance, start with your existing policies.

Most insurers require minimum liability limits on your home and auto policies before the umbrella coverage can activate. These requirements ensure the base layer of protection is strong enough.

The easiest approach is to bundle the umbrella policy with your existing coverage. Many insurers offer meaningful multi-policy discounts when everything sits under one provider.

An independent insurance agent who works with high-net-worth clients can review your current limits and recommend adjustments if necessary.

The process is usually straightforward. But the financial protection it provides can be enormous.

Protecting Wealth Is Easier Than Rebuilding It

Building wealth takes decades of work, discipline, and smart decisions.

Losing it can happen far faster.

A single accident.

A lawsuit tied to an employee.

An online comment that spirals into a defamation claim.

Any of those scenarios can trigger financial exposure far beyond the limits of standard insurance policies.

Umbrella insurance doesn’t eliminate risk. Nothing does.

What it does is prevent a legal judgment from turning into a financial catastrophe.

For high-net-worth individuals in 2026, that extra layer of protection isn’t a luxury.

It’s basic financial defense.