The Ultimate Guide to Maximizing Your 401(k) Employer Match in 2026

As a Certified Financial Planner (CFP®), I see the same story every year: brilliant professionals who master their crafts but let their greatest wealth-building engine idle in the driveway.

In the landscape of the best retirement plans 2026 has to offer, the 401(k) remains the undisputed heavyweight champion. Why? Because of the employer match. It is quite literally the only place in the financial world where you receive a guaranteed, 100% return on your investment before the money even touches the market.

If you aren’t capturing your full match, you aren’t just missing a “perk”—you are taking a voluntary pay cut. Let’s break down how to optimize your strategy for the current year.

How Employer Match Formulas Actually Work

To win the game, you have to understand the scoreboard. Most companies use one of two structures for their employer match calculation.

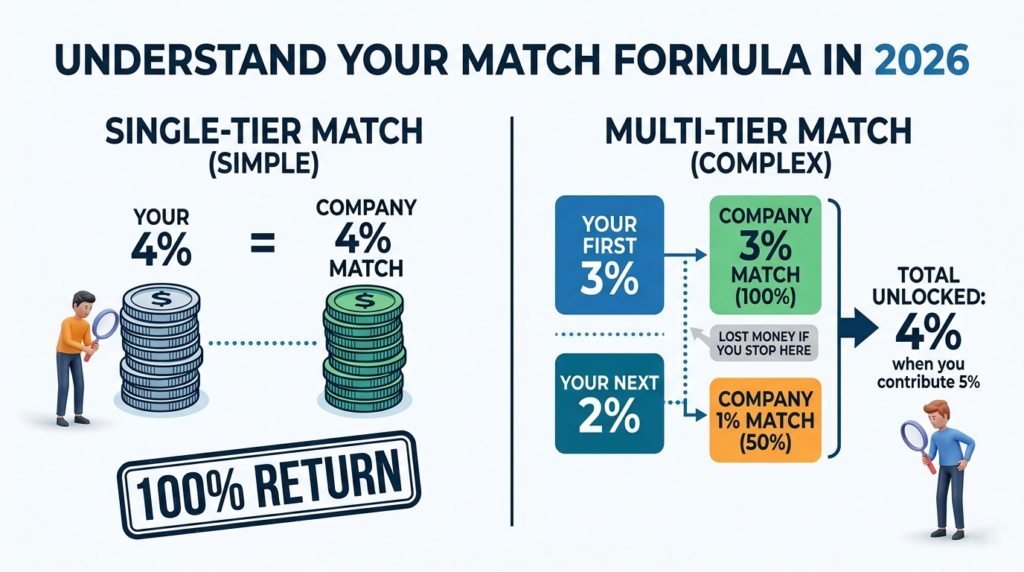

1. The Single-Tier Match (The Dollar-for-Dollar)

This is the gold standard. Your employer matches 100% of your contributions up to a specific percentage of your salary (usually 3% to 6%).

- Example: You earn $100,000 and the match is 4%. You contribute $4,000; the company chips in $4,000. Your total starting balance is $8,000.

2. The Multi-Tier Match (The “Partial” Match)

This is where many professionals leave money on the table because the math is slightly more deceptive. A common formula is: “100% match on the first 3%, and 50% match on the next 2%.”

- The Trap: If you only contribute 3%, you get a 3% match. But to get the full benefit, you must contribute 5% to unlock that final 1% of company money.

CFP Pro-Tip: Always check your Summary Plan Description (SPD). If your auto-enrollment was set at 3%, but the full match requires 6%, you are leaving thousands of dollars behind every single year.

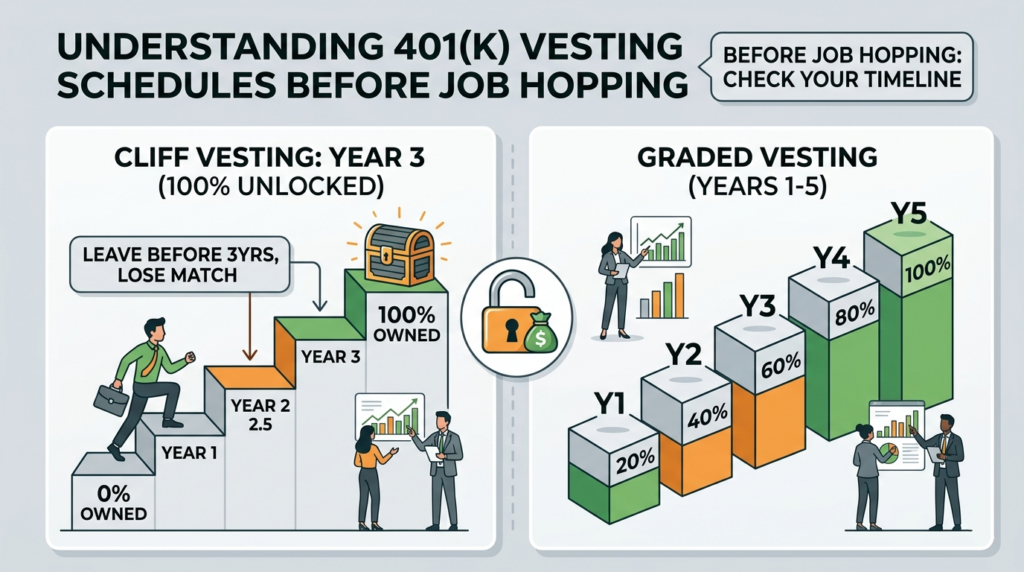

Understanding Vesting: The “Golden Handcuffs”

In an era of frequent job hopping, understanding vesting is the difference between retiring wealthy and leaving empty-handed. Vesting is the timeline that determines when you actually own the money your employer contributed.

- Employee Contributions: You always own 100% of the money you put in.

- Employer Match: This is subject to a schedule.

Common Vesting Schedules in 2026:

- Cliff Vesting: You own 0% of the match until you hit a specific milestone (e.g., 3 years), at which point you jump to 100%. If you leave at year 2.9, the company takes back every cent of their match.

- Graded Vesting: You gain ownership gradually (e.g., 20% per year). By year five, you are fully vested.

Strategic Move: Before you sign that resignation letter for a new role, check your vesting date. Sometimes staying an extra three weeks can save you $20,000 in unvested employer matches.

What’s New in 2026: IRS Limits and Policy Shifts

The IRS has adjusted the 401k contribution limits for 2026 to account for persistent cost-of-living adjustments. Staying within these guardrails is essential for tax efficiency.

2026 Contribution Caps:

- Individual Deferral Limit:$24,500 (This is the “pre-tax” or “Roth” limit for employees).

- Catch-up Contribution:$8,000 (For those aged 50 and older).

- Total Section 415 Limit:$72,000 (This includes your contributions + employer match + profit sharing).

The SECURE Act 2.0 “Super Catch-Up”

A critical nuance for 2026: If you are aged 60, 61, 62, or 63, your catch-up limit is increased to the greater of $10,000 or 150% of the standard catch-up. For 2026, this “super catch-up” sits at $11,250.

Mandatory Roth Catch-Ups

If you earned more than $145,000 (indexed to $150,000 for 2026) in the previous year, the IRS now mandates that your catch-up contributions must be Roth. This means you pay taxes on that $8,000 now, but it grows tax-free forever.

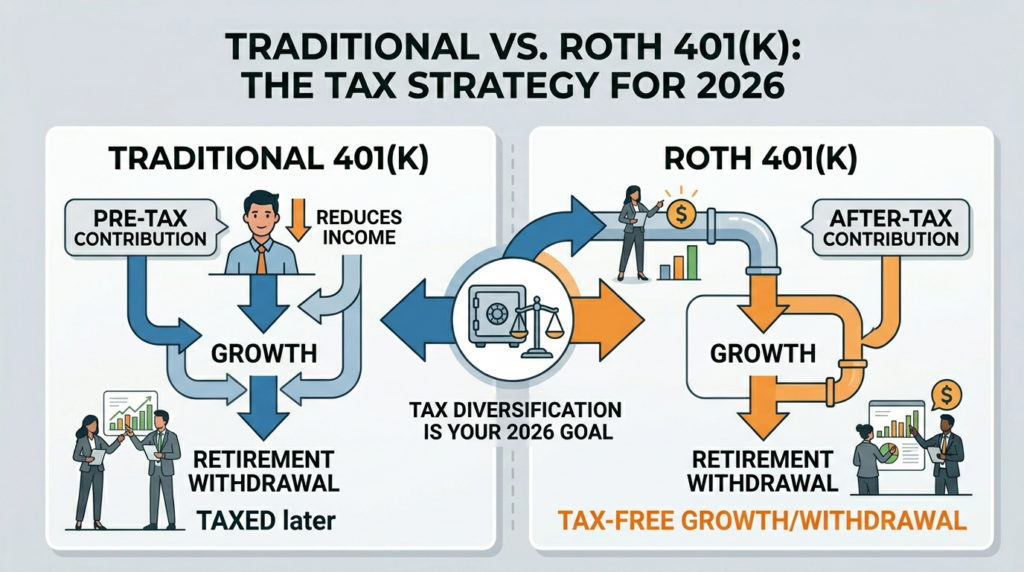

Traditional vs. Roth 401(k): The 2026 Debate

Choosing between a Traditional vs. Roth 401k is the most common question I receive.

- Traditional 401(k): You get a tax break today. Your $24,500 contribution lowers your taxable income for 2026. You pay taxes when you withdraw in retirement.

- Roth 401(k): You pay taxes today. Your contribution doesn’t lower your current tax bill, but every dollar of growth and every withdrawal in retirement is 100% tax-free.

Retirement Investment Advice: If you are early in your career and in a lower tax bracket, Roth is usually the winner. If you are in your peak earning years (32% tax bracket or higher), the immediate tax savings of a Traditional 401(k) might be more beneficial.

The Trap of Early Withdrawal: Protect Your Future Self

I cannot stress this enough: your 401(k) is not a high-yield savings account. It is a locked vault. If you tap into these funds before age 59.5, the financial carnage is severe.

- The 10% Penalty: The IRS takes 10% right off the top for early distribution.

- Ordinary Income Tax: The withdrawal is added to your 2026 income. If you’re in the 24% bracket, you’ve now lost 34% of your money before you even see it.

- Mandatory Tax Withholding: By law, employers must withhold 20% of early distributions for federal taxes. You might ask for $50,000 and only receive $35,000 in your bank account, yet you still owe the full tax bill at year-end.

If you are in a genuine crisis, look into a 401(k) Loan instead. You pay the interest back to yourself, and as long as you remain employed, you avoid the taxes and penalties.

Conclusion: Designing Your 2026 Roadmap

Maximizing your 401(k) is the foundation of a sophisticated financial plan. To recap your 2026 strategy:

- Contribute at least enough to get the full employer match. Anything less is leaving free money on the table.

- Audit your vesting schedule before making any career pivots.

- Maximize the new 2026 limits ($24,500) if your cash flow allows.

- Diversify your tax buckets by utilizing both Traditional and Roth options.

Every individual’s tax situation is unique. While these rules provide the framework, the “optimal” move depends on your total household income, debt-to-equity ratio, and long-term legacy goals.