Term vs. Whole Life Insurance: Calculating Your Coverage Gap in 2026

Life insurance in 2026 isn’t something you buy once and forget about. It’s closer to a financial safety system—one designed to protect your family from two uncomfortable but very real possibilities: dying earlier than expected or living longer than your money lasts.

Both risks are expensive.

Choosing the right policy means understanding how the two main types of life insurance actually work. Not the marketing version. The real mechanics.

Because once you see how term life and whole life insurance behave financially, the decision becomes much clearer.

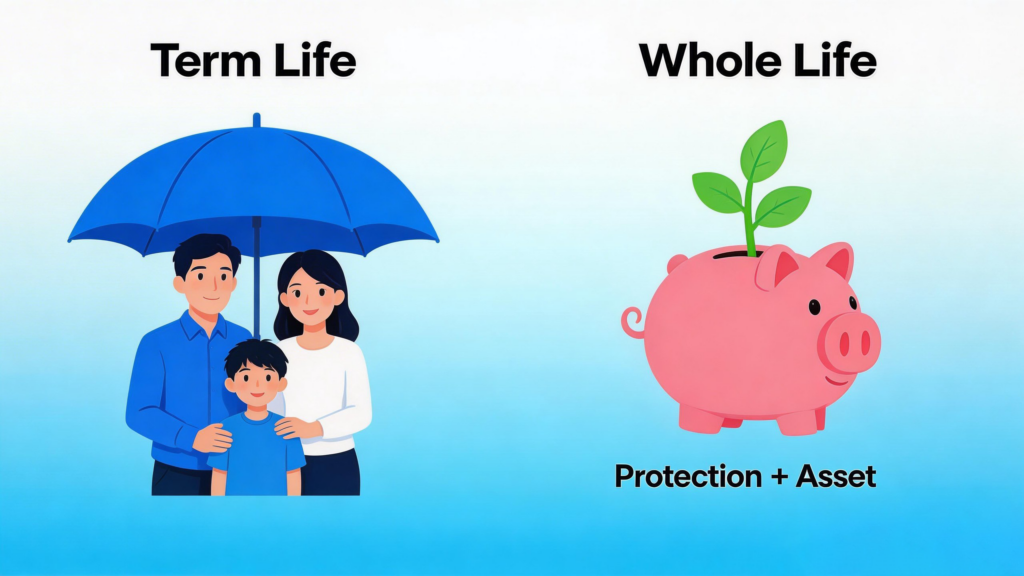

Term Life Insurance: Pure Protection Without the Complexity

Let’s start with the simplest option.

Term life insurance exists for one purpose: protection during a specific period of time. You choose a coverage length—typically 10, 20, or 30 years—and pay a fixed monthly premium. If you die during that window, the insurance company pays your beneficiaries a tax-free death benefit.

If the policy expires and you’re still alive? The coverage ends.

That’s it.

In practice, term insurance functions a lot like homeowners or auto insurance. You’re paying to protect against a financial catastrophe.

Which is why many families start their search with phrases like “best term life insurance 2026.” Budgets are tight, housing costs remain high, and parents want the maximum financial protection they can get for every premium dollar.

Term policies deliver exactly that.

A healthy 35-year-old, for example, can often secure $1 million of coverage for surprisingly little—sometimes less than the cost of a monthly streaming subscription or gym membership.

That’s why term insurance dominates among young families.

But it isn’t the only option.

Whole Life Insurance: Protection That Also Builds an Asset

Now let’s shift gears.

Whole life insurance operates very differently from term policies. Instead of temporary coverage, it’s a permanent contract that remains active for your entire lifetime—as long as premiums are paid.

In most modern policies, coverage lasts until age 121.

But permanence isn’t the feature that attracts wealthier policyholders. The real draw is the policy’s cash value component.

Here’s how that works.

Each premium payment gets split into two parts:

One portion funds the insurance protection

The other portion flows into a tax-deferred cash value account

Over time, that internal account grows steadily. It accumulates value based on guarantees from the insurer and, in many cases, additional dividend performance.

High-net-worth investors often analyze this growth using a whole life insurance cash value calculator. The goal isn’t just insurance coverage—it’s portfolio stability.

Think of it this way.

Market investments swing wildly during economic shocks. Whole life cash value, by contrast, grows in a slow, predictable pattern. For some investors, that predictable growth acts as a volatility buffer inside a broader financial strategy.

Not flashy. But reliable.

Cost Structure: Predictable vs. Expensive

Of course, that stability comes at a price.

Term life insurance is inexpensive because the coverage is temporary and most policyholders outlive the term. Whole life insurance, on the other hand, guarantees a payout eventually. That guarantee requires significantly higher premiums.

The difference can be dramatic.

A $1 million term policy for a 35-year-old might cost $40 to $70 per month. A comparable whole life policy could easily exceed $700 per month depending on the structure.

That gap explains why term insurance often dominates search trends such as “affordable life insurance for parents.”

Families dealing with mortgages, childcare costs, and rising groceries usually need maximum protection—not long-term cash value accumulation.

But that doesn’t mean whole life has no place.

It simply serves a different financial objective.

The Real Question: How Much Coverage Do You Actually Need?

Many people get stuck comparing policy types without answering the more important question.

How much life insurance should you carry in the first place?

Here’s the uncomfortable truth: the coverage amounts people purchased ten years ago often aren’t enough anymore.

Inflation has changed the math.

A $500,000 policy that looked massive in 2016 doesn’t stretch nearly as far in 2026. College tuition alone tells the story. Private universities now average more than $65,000 per year, and home prices remain near historic highs in many regions.

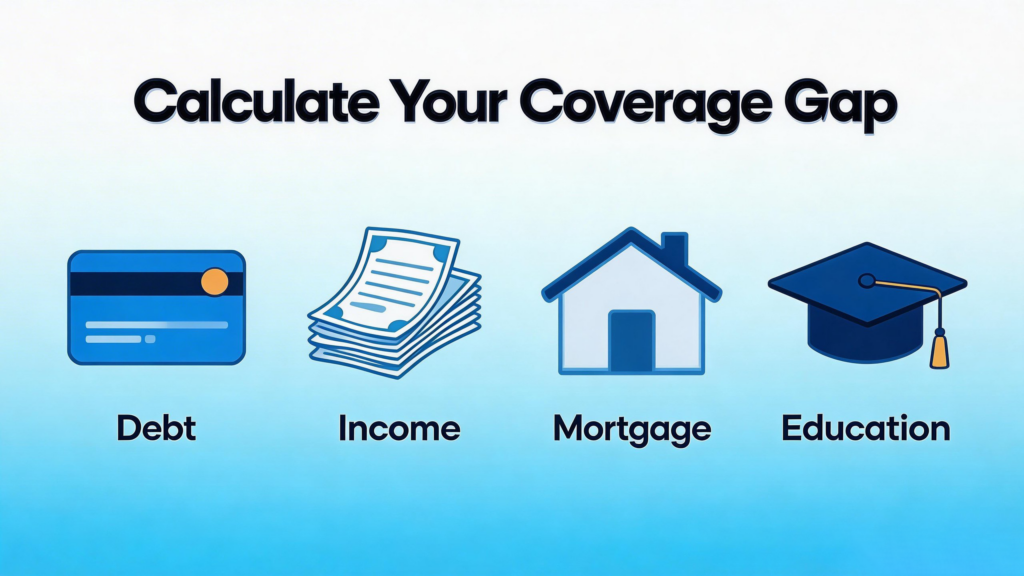

That’s why many advisors rely on a simple framework called the DIME Formula.

It helps estimate a realistic protection target.

D — Debt

Start with every non-mortgage liability your family carries:

- Credit cards

- Car loans

- Student loans

- Personal loans

These balances shouldn’t survive you.

I — Income Replacement

Next, calculate how long your family would need financial support.

Most planners recommend replacing 10 to 15 years of income. If you earn $80,000 annually, your income protection need alone may exceed $800,000.

M — Mortgage

Add the full payoff amount of your home loan. Eliminating the mortgage prevents your family from facing housing insecurity during an already difficult time.

E — Education

Finally, estimate future education costs for each child. College expenses continue climbing, and many parents want those goals protected regardless of what happens.

Spotting the Coverage Gap

Once you total your DIME number, compare it against your existing policies.

This is where many people experience an unpleasant surprise.

Employer-provided life insurance—while helpful—often covers only one or two times your annual salary.

Let’s say your DIME calculation lands at $1.2 million.

Your workplace benefit might only provide $200,000.

That leaves a $1 million coverage gap.

Closing that gap is usually easier than people expect. Searching for affordable life insurance for parents often reveals surprisingly low premiums for healthy applicants.

The bigger risk isn’t cost.

It’s procrastination.

The Quiet Revolution in Life Insurance Underwriting

Another reason life insurance has become easier to purchase: the approval process has changed dramatically.

A decade ago, buying coverage often meant scheduling a medical exam, waiting for blood work, and enduring weeks of underwriting review.

Those days are fading.

Many insurers now rely on Accelerated Underwriting (AU) systems powered by predictive algorithms. Instead of drawing blood, carriers analyze your digital health footprint—data pulled from prescription records, driving history, and actuarial risk databases.

If the data looks clean, approval can happen quickly.

Sometimes instantly.

Policies offering no-medical-exam coverage are now widely available for applicants in good health, even for policies reaching seven-figure death benefits.

Of course, speed raises another concern: privacy.

Current U.S. insurance regulations restrict how this information can be used. Insurers may analyze data strictly for risk assessment, not for resale to advertisers or unrelated third parties.

So while the process is faster, safeguards still exist.

Choosing the Right Strategy in 2026

Different life stages call for different insurance strategies. There isn’t a universal answer.

But some patterns show up repeatedly.

Young Families (Ages 25–45)

Term life insurance almost always wins here.

Debt levels are high. Mortgages are new. Kids are young. Liquid assets are still building. Families in this stage need large protection amounts at manageable prices.

A 30-year term policy often provides the right bridge until children become financially independent and major debts disappear.

High-Net-Worth Individuals and Business Owners

This group often blends both policy types.

Term coverage handles large immediate risks—business obligations, estate liquidity, or partnership protection. Whole life policies serve a different role. Their cash value can provide tax-efficient liquidity, estate planning advantages, or emergency capital.

Used strategically, whole life becomes less about insurance and more about financial engineering.

Empty Nesters and Pre-Retirees (Ages 55+)

At this stage, massive coverage amounts usually aren’t necessary.

Mortgage balances shrink. Children move out. Retirement savings grow.

However, smaller permanent policies still serve useful purposes. Some retirees use whole life to guarantee funeral expenses are covered. Others structure policies as a predictable inheritance for grandchildren.

The goal shifts from protection to legacy.

One Final Reality Check

The most expensive life insurance policy isn’t the one with the highest premium.

It’s the one someone meant to buy—but never actually purchased.

In 2026, evaluating life insurance has become easier than ever. Online tools allow you to compare life insurance quotes, calculate your coverage gap, and even model future policy performance with tools like a whole life insurance cash value calculator.

But those tools only matter if you use them.

The first step is simple: review your current coverage against today’s cost of living. Run the numbers. See where you stand.

Because the real risk isn’t choosing the wrong policy.

It’s leaving your family unprotected while assuming everything is fine.