Pet Insurance for Senior Dogs in 2026: What Owners Actually Need to Know

Veterinary care isn’t cheap anymore—and in 2026, the price gap is widening. Clinics are investing in advanced imaging, specialized surgeons, and cutting-edge diagnostics. Think high-field MRIs, cardiology consults, oncology treatment plans. Impressive medicine. Expensive medicine.

That reality hits dog owners hardest when their pet crosses a certain age threshold. Around seven or eight years old—earlier for large breeds—most dogs officially enter their senior years. And that’s when the financial risk changes.

A young dog might visit the vet for a rash or an ear infection. A senior dog? Arthritis, heart disease, cancer screenings, ligament tears. Entirely different level of care.

So when people search for the best pet insurance for senior dogs, they’re not just browsing policies. They’re trying to protect themselves from the kind of vet bill that shows up once—and wrecks a monthly budget.

Let’s break down what the landscape actually looks like in 2026.

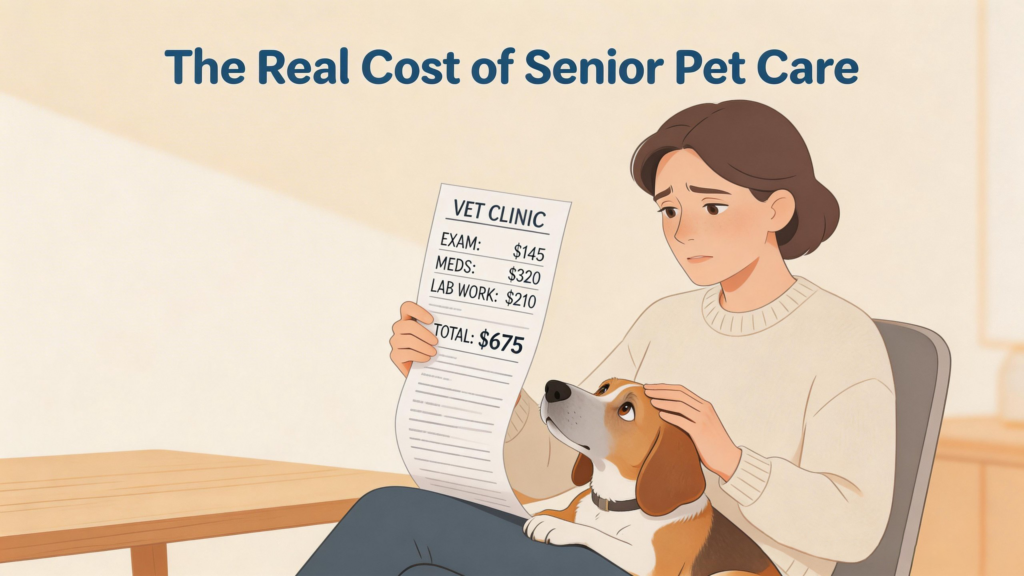

The Real Cost of Aging Dogs in 2026

If you’ve had a senior dog before, you already know the pattern. Health issues don’t appear gradually. They arrive in clusters.

One month everything seems normal. A few weeks later you’re scheduling orthopedic consultations and blood panels.

Here’s what typical treatment costs look like across the United States right now:

Osteoarthritis management: $1,200–$2,500 per year. That includes joint supplements, physical therapy sessions, and injectable treatments like Librela.

Cruciate ligament (CCL) surgery: $4,500–$7,000 for one knee. And yes—dogs often tear the second ligament later.

Tumor removal surgery: $1,500–$4,500 depending on location and pathology results.

Chronic kidney disease (CKD): $2,000–$5,000 annually for diagnostics, prescription diets, medications, and fluid therapy.

Heart disease treatment: Initial diagnostic workups average around $1,500. After that, medications such as Pimobendan can easily exceed $200 per month.

Add it up and the numbers escalate quickly.

Veterinarians estimate that roughly 80% of dogs over age eight will develop at least one chronic health condition. Sometimes two. Occasionally three.

That’s why more owners are researching affordable life insurance for pets before problems appear. Once symptoms start showing, insurance options shrink fast.

The Pre-Existing Condition Problem

If you ask experienced dog owners what the biggest frustration with pet insurance is, they’ll almost always mention the same phrase:

Pre-existing conditions.

Insurance companies define a pre-existing condition as any illness or injury that showed symptoms—or was documented by a veterinarian—before the policy became active.

In other words, if your dog already has the problem, insurance won’t cover it.

Sounds simple. In practice, it gets complicated.

The good news is that many insurers in 2026 have refined how they classify these conditions. Providers such as Lemonade, Spot Pet Insurance, and Pumpkin Pet Insurance now separate issues into two categories: curable and incurable.

And that distinction matters.

Conditions Insurance Will Not Cover

Some diagnoses permanently fall outside insurance protection if they existed before enrollment.

Common examples include:

- Diabetes

- Chronic allergies

- Hip dysplasia

- Long-term endocrine disorders

Once these conditions appear in a medical record, coverage for related treatment is essentially off the table.

That’s why timing matters. Waiting until a dog shows symptoms before purchasing insurance almost always backfires.

The “Curable Condition” Loophole

Here’s something many pet owners don’t realize.

Certain health problems are considered temporary by insurers. If they resolve completely—and stay resolved for a specific period—they can be covered again later.

Typical examples include:

- Respiratory infections

- Minor gastrointestinal illness

- Ear infections

- Small injuries

Most insurers apply what’s known as a look-back period, usually between 180 days and 12 months. If the dog remains symptom-free during that window, a future recurrence may be treated as a new condition.

It’s not guaranteed. But it can make a major difference.

Pro tip: After purchasing a policy, immediately request a full medical record review. This forces the insurer to evaluate your dog’s history and confirm which conditions they currently consider pre-existing.

Without that review, some owners only discover exclusions when they file their first claim. That’s a terrible moment to learn the fine print.

Waiting Periods: The Detail Owners Miss

Another piece of the puzzle is the waiting period.

Insurance never activates instantly.

Most accident coverage begins within two or three days. Illness coverage typically starts after about two weeks.

But orthopedic issues follow a completely different timeline.

Many policies still enforce six-month waiting periods for conditions like:

- Cruciate ligament injuries

- Hip dysplasia

- Patellar luxation

And here’s where things get frustrating.

If your dog develops a limp during that waiting period—even once—future treatment for that leg may be permanently excluded.

Yes, permanently.

Some insurance companies allow you to shorten or waive this orthopedic waiting period if your veterinarian performs a specialized orthopedic exam within the first 30 days of the policy.

For large breeds or older dogs, that exam is absolutely worth doing.

Choosing the Right Coverage for an Older Dog

Insuring a senior dog will always cost more than insuring a puppy. There’s no way around that.

But you can control how the policy is structured.

Think of pet insurance as a system with three adjustable settings: reimbursement rate, deductible, and annual coverage limit.

Adjusting those settings changes both your monthly premium and the protection level.

- Reimbursement Percentage

This determines how much of the bill the insurer pays after your deductible.

Common options include:

- 90% reimbursement: Maximum protection, but higher premiums.

- 80% reimbursement: A balanced option for many owners.

- 70% reimbursement: Lower monthly cost while still covering most large expenses.

For senior dogs, the 70–80% range often hits the sweet spot between affordability and real protection.

- Annual Deductible

The deductible is what you pay before insurance begins covering expenses.

Higher deductibles reduce the monthly premium.

For older dogs, many owners intentionally choose a deductible between $750 and $1,000.

Why? Because insurance works best when it protects against catastrophic events—major surgeries, cancer treatment, chronic disease—not routine $200 vet visits.

- Annual Coverage Limits

This is the maximum amount the insurer will pay each year.

And this is where many policies fall short.

Plans capped at $5,000 per year can disappear surprisingly fast. A single emergency surgery or cancer treatment plan can exhaust that limit almost immediately.

For senior dogs, experts increasingly recommend:

- Unlimited annual coverage, or

- At least a $10,000 annual limit

It costs more upfront. But it prevents unpleasant surprises later.

One Last Reality Check

Insurance for older dogs is all about timing.

Veterinary records matter. A single note from your vet—something as minor as “mild stiffness” or “early cloudiness in eyes”—can later be interpreted as the first sign of arthritis or cataracts.

Once that happens, insurers may classify the condition as pre-existing.

That’s why proactive enrollment is critical.

If coverage isn’t possible right now and a large vet bill appears, temporary financing options like CareCredit or Scratchpay can help spread out payments. Just remember: those are loans, not insurance.

They solve today’s bill, not tomorrow’s diagnosis.

The smarter strategy is simpler.

Get the insurance before the limp appears. Before the bloodwork changes. Before the X-ray reveals something unexpected.

Because once those records exist, the window closes fast.