Medicare Part B vs. Medicare Advantage: 2026 Coverage Updates

Understanding the Stakes in 2026

Here’s the hard truth: the wrong choice can drain your retirement savings faster than you think. It’s not just about premiums. Out-of-pocket expenses, provider networks, prescription coverage—these factors can create a perfect storm if ignored. Understanding your options now can save thousands down the road.

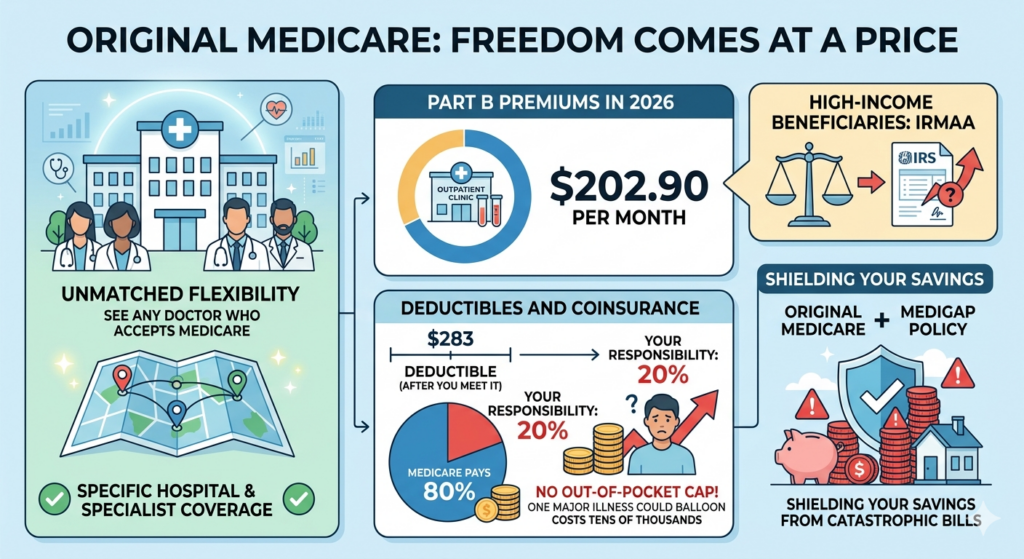

Original Medicare: Freedom Comes at a Price

Original Medicare still offers unmatched flexibility. Want to see any doctor who accepts Medicare? No problem. Need a specific hospital or specialist? You’re covered. But freedom isn’t free.

- Part B Premiums in 2026

The standard Part B premium is $202.90 per month. That covers outpatient visits, lab tests, and durable medical equipment. But beware—high-income beneficiaries may pay more through the Income-Related Monthly Adjustment Amount (IRMAA). This isn’t optional; the IRS enforces it automatically.

- Deductibles and Coinsurance

The 2026 Part B deductible is $283. After you meet it, Medicare pays roughly 80% of approved amounts. The remaining 20%? That’s your responsibility. There’s no out-of-pocket cap. One major illness could balloon costs tens of thousands.

This is why many seniors combine Original Medicare with a Medigap policy. These supplemental plans fill the gaps, capping what you owe and shielding your savings from catastrophic medical bills.

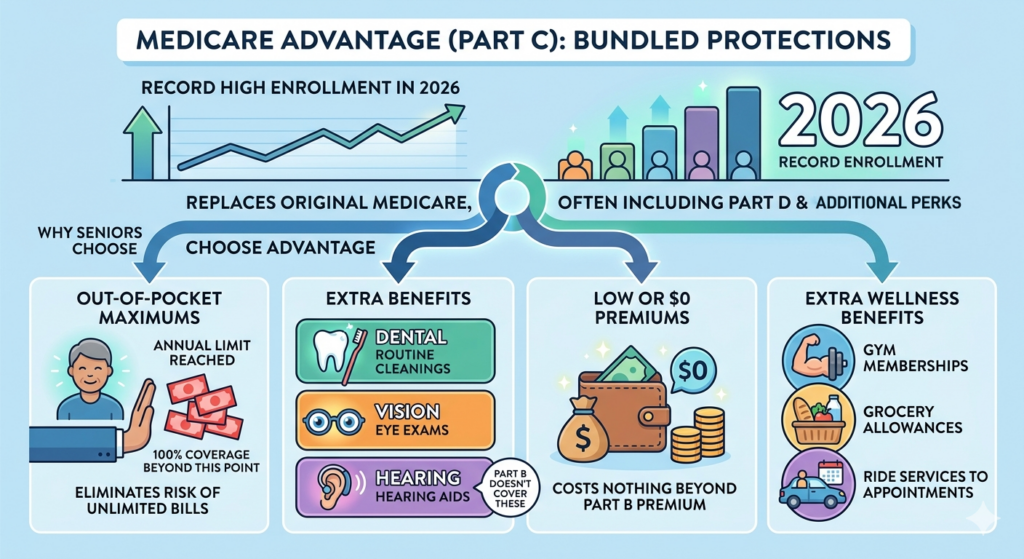

Medicare Advantage: Bundled Protections

Medicare Advantage (Part C) plans have exploded in popularity. By 2026, enrollment is at record highs. These privately managed plans replace Original Medicare, often including Part D (prescription drugs) and additional perks.

Why Seniors Are Choosing Advantage

The appeal is clear. Part C offers:

- Out-of-Pocket Maximums: Once you hit your annual limit, the plan covers 100% of care. This eliminates the risk of unlimited bills.

- Dental, Vision, and Hearing: Routine cleanings, eye exams, and hearing aids are often included. Part B doesn’t cover these.

- Low or $0 Premiums: Many plans cost nothing beyond your Part B premium.

- Extra Wellness Benefits: Think SilverSneakers gym memberships, grocery allowances for chronic conditions, or ride services to appointments.

The convenience and safety nets make Advantage plans attractive for those willing to stay in-network.

The Annual Election Period: What to Watch

The Annual Election Period (AEP) is when your choices really matter. In 2026, insurers are adjusting benefits aggressively. Ignore the details, and you could pay more or lose coverage for preferred doctors.

- Review Your ANOC (Annual Notice of Change): Changes in premiums, copays, and drug formularies happen every September. Don’t skim—these details can dramatically affect your costs.

- Check Provider Networks: Some Advantage plans have narrowed networks. Confirm your specialists and preferred hospitals are still in-network.

- Scrutinize Prescription Lists: If your medications jump to a higher tier, costs could spike unexpectedly.

- Evaluate Extra Benefits: If you never use the gym stipend or vision care, maybe you’d prefer lower copays elsewhere.

Choosing Between Part B and Advantage: Key Factors

This isn’t a one-size-fits-all decision. Three main variables should guide your choice:

- Travel and Flexibility

- Original Medicare + Medigap: Best for snowbirds or frequent travelers. Accepted almost everywhere in the U.S. that accepts Medicare.

- Medicare Advantage: Works if you primarily seek care locally and can stay in-network.

- Health Status and Predictability

- Original Medicare + Medigap: Ideal for chronic conditions and frequent specialist visits. Predictable costs, minimal surprises.

- Medicare Advantage: Suitable for relatively healthy seniors wanting lower premiums and extra perks.

- Budget and Risk Tolerance

- Original Medicare + Medigap: You “pay upfront” with higher premiums to avoid unpredictable out-of-pocket expenses.

- Medicare Advantage: Lower monthly payments, copays for each visit, but with a safety net through the annual out-of-pocket maximum.

Medigap vs. Advantage: When You Need Both

Many beneficiaries combine Original Medicare with Medigap to cap costs while keeping flexibility. Others prefer the “all-in-one” Advantage route, accepting network limits for convenience and built-in coverage perks.

The smart approach? Analyze your lifestyle, anticipated healthcare needs, and risk tolerance. There’s no shame in switching if your situation changes—2026 rules allow reassessment during open enrollment.

Strategic Tips for 2026 Enrollment

- Organize Your Medical Records: Make a list of medications, specialists, and past procedures. It helps when comparing networks and formularies.

- Compare Costs, Not Just Premiums: A low monthly premium doesn’t guarantee low total costs. Deductibles, copays, and prescription tiers matter.

- Look at Local Networks: A plan that’s highly rated nationally may exclude your preferred local providers.

- Consult an Independent Agent: Licensed agents can provide side-by-side comparisons and explain nuances. They can help you spot changes that matter before you commit.

Fall is not the time to procrastinate. Waiting until January could cost you coverage, money, or both.

The Bottom Line: Protecting Your Health and Savings

Medicare in 2026 demands active decision-making. Original Medicare offers unmatched flexibility but carries financial risk without Medigap. Medicare Advantage bundles benefits and out-of-pocket protections but limits your provider choices.

Your goal is simple: quality care without financial devastation. Act intentionally. Review your ANOC, confirm networks, weigh premiums versus coverage, and plan for potential medical events.

The smartest move is proactive engagement. Don’t let complexity, advertising, or inertia decide your healthcare future. Compare plans, ask questions, and secure coverage that aligns with your lifestyle, health, and retirement goals.

In 2026, Medicare isn’t just a government program—it’s a critical financial decision. Make it work for you.