Debt Consolidation Loans for Fair Credit in 2026: Rates, Risks, and When the Math Actually Works

If you’re juggling multiple credit card balances, you already know the feeling. One payment due on the 3rd, another on the 12th, two more before the end of the month. Every card has a different interest rate. None of them are low.

At some point people start looking for a reset.

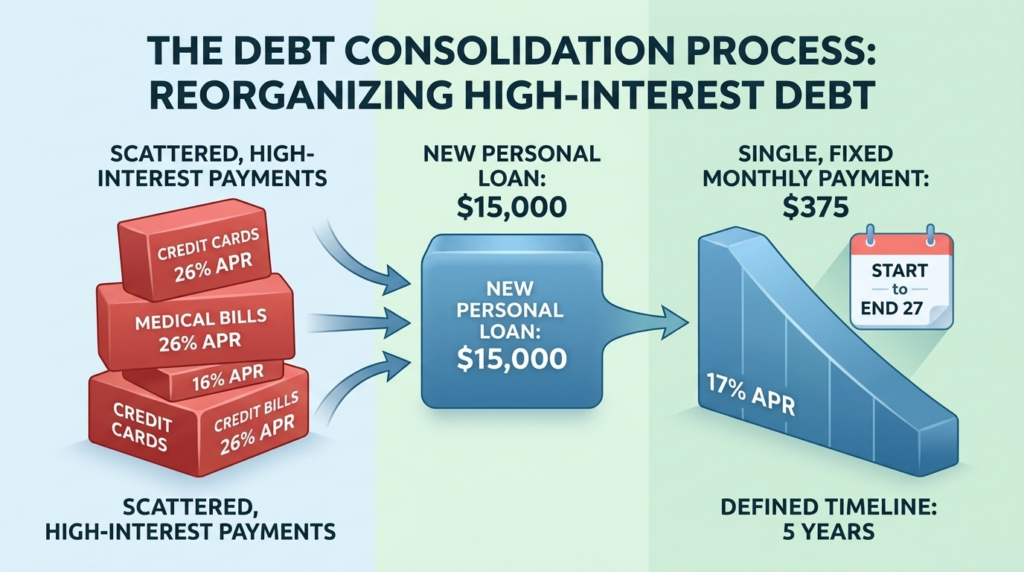

That’s essentially what a debt consolidation loan is meant to do. You take out a single personal loan and use it to wipe out several high-interest balances—usually credit cards, sometimes medical bills or smaller personal loans. Instead of managing a pile of accounts, you’re left with one fixed monthly payment and a defined payoff timeline.

Simple in theory. But in 2026, the details matter more than ever—especially if your credit score sits somewhere in the “fair credit” range.

What Debt Consolidation Really Means

Let’s strip away the marketing language.

Debt consolidation doesn’t eliminate debt. It reorganizes it.

You borrow money from a lender, typically through a personal loan. That loan pays off your existing balances. The old accounts close or drop to zero, and you repay the new loan over a fixed term—often 36 to 60 months.

That structure alone changes the psychology of repayment.

Credit cards are revolving debt. Minimum payments keep them alive indefinitely. You can carry a balance for decades if you only pay the minimum.

A personal loan is different. It has a start date and an end date. When the final payment posts, the debt disappears. No revolving balance waiting to grow again.

That’s why many borrowers searching for best debt consolidation loans for fair credit start with this option. Not because it’s magic. Because it introduces structure.

The 2026 Interest Rate Landscape for Fair Credit

Now let’s talk numbers.

As of March 2026, the Federal Reserve has kept benchmark rates relatively steady. Lending markets, however, remain cautious. Personal loan lenders are pricing risk carefully—especially for borrowers with mid-range credit profiles.

If your credit score sits around 650, most personal loan offers will land somewhere between 14% and 19% APR.

At first glance, that doesn’t sound cheap.

But compare it to the average credit card interest rate in 2026. Many cards now charge 26.99% APR or higher, particularly for balances that have rolled over month after month.

That spread—roughly ten percentage points—creates the opportunity for consolidation savings.

And the math can be dramatic.

A Real-World Debt Consolidation Example

Imagine a household carrying $15,000 in credit card debt spread across several accounts.

Typical credit card APR: 26%

If that borrower sticks to minimum payments, the timeline can stretch well beyond a decade. Interest alone can exceed the original balance.

Now shift the same $15,000 into a 5-year personal loan at 17% APR.

Two big things change:

The repayment schedule becomes fixed.

The interest rate drops significantly.

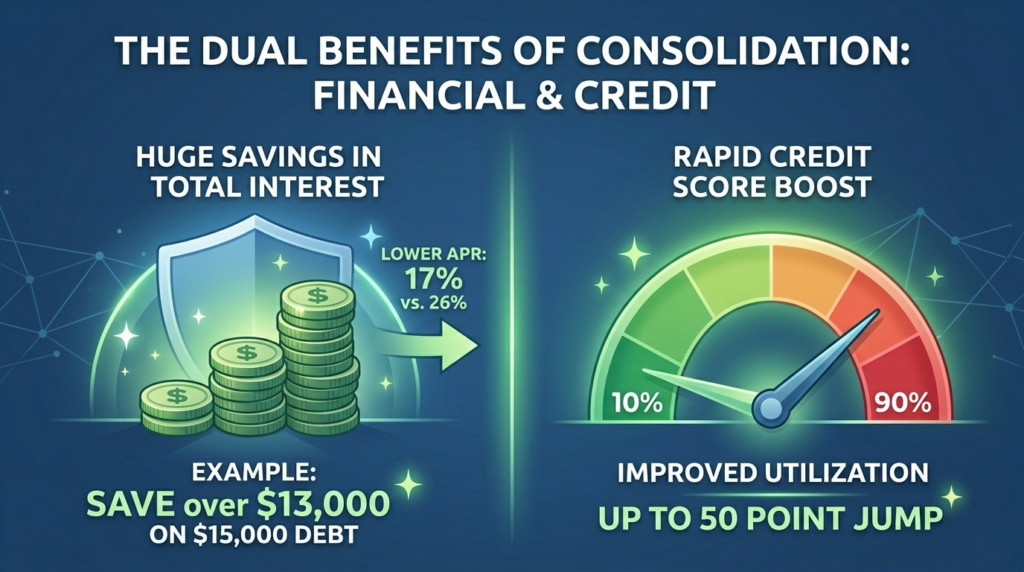

Over the life of the loan, that borrower could save more than $13,000 in interest and eliminate the debt years earlier.

That’s why people frequently search for personal loan rates for a 650 credit score. For many households, consolidation is the first step toward actually getting out of debt instead of just servicing it.

Still, the strategy isn’t flawless.

The Real Advantages of Debt Consolidation

When consolidation works, it works for very practical reasons.

Financial Simplicity

Multiple debts create friction. Payments get missed. Interest compounds.

A consolidation loan reduces everything to one monthly payment. Same amount. Same due date. Less room for error.

For borrowers who’ve been dealing with four or five accounts, that change alone can stabilize their finances.

Lower Total Interest

Interest rate differences may look small on paper. Over several years, they become enormous.

Moving balances from a 25% credit card to a 17% personal loan cuts the cost of borrowing dramatically.

It’s not about getting a “cheap” loan. It’s about getting a cheaper one.

A Defined Exit Strategy

Revolving credit has no finish line.

Installment loans do.

Whether the term is 36 months or 60 months, the borrower knows exactly when the debt disappears—assuming payments stay on schedule.

That psychological clarity matters more than most lenders admit.

The Downsides Borrowers Often Overlook

Debt consolidation is useful. It is not a cure.

Several risks show up again and again.

Origination Fees

Many lenders charge an upfront origination fee, especially for borrowers with fair credit.

These fees typically range from 1% to 5% of the loan amount and are deducted before the funds reach your account.

Borrow $15,000, and you might receive $14,250 after fees.

That doesn’t necessarily make the loan a bad deal, but it does affect the total cost.

The “Double Debt” Problem

This is the biggest danger—and it happens constantly.

A borrower uses a consolidation loan to pay off credit cards. The balances drop to zero.

Then spending resumes.

Six months later the borrower has a personal loan payment plus new credit card balances.

Debt consolidation only works when spending behavior changes alongside the loan.

Otherwise it becomes a temporary reshuffling of debt.

Credit Score Impact

Most lenders allow borrowers to pre-qualify with a soft credit pull, meaning the initial rate check doesn’t affect your credit score.

But once you submit a full application, the lender will run a hard inquiry.

That inquiry can temporarily reduce your score by a few points.

For most borrowers the impact fades quickly, but it’s worth understanding ahead of time.

Why Consolidation Can Improve Your Credit Score

Here’s something many borrowers don’t realize: consolidation can actually boost your credit score relatively quickly.

The key factor is credit utilization.

Credit utilization measures how much of your available credit card limit you’re using. High utilization signals risk to credit scoring models.

For example:

- Total credit card limits: $20,000

- Current balances: $18,000

Your utilization rate is 90%. That’s extremely high.

If you consolidate that debt into a personal loan, your credit card balances drop close to zero. Utilization might fall from 90% to under 10% overnight.

Because personal loans are categorized as installment debt, they don’t affect utilization ratios in the same way.

Many borrowers with fair credit see their scores rise 20 to 50 points within a couple of billing cycles after consolidating.

It’s one of the fastest ways to improve credit utilization without paying down the balance slowly over time.

Red Flags: How to Avoid Predatory Loans in 2026

Not every lender operates in the borrower’s best interest. High-interest environments attract questionable offers.

When comparing debt relief options in 2026, watch for several warning signs.

The 36% APR Rule

Consumer advocates widely agree on a basic guideline: any personal loan with an APR above 36% is considered predatory.

At that level, interest compounds so aggressively that repayment becomes extremely difficult.

Reputable lenders stay below this threshold.

Prepayment Penalties

A good loan should reward early repayment—not punish it.

If a lender charges a fee for paying off your loan early, take that as a warning sign. Most mainstream lenders have eliminated these penalties.

“Guaranteed Approval” Advertising

No legitimate lender guarantees approval without reviewing your credit profile.

If a company promises instant approval regardless of your score, the catch usually appears later—in the form of massive interest rates or hidden fees.

A Smarter Strategy for Borrowers with Fair Credit

If your credit score falls between 600 and 700, the smartest move is simple: pre-qualify before applying.

Many fintech lenders now allow borrowers to check loan offers using a soft credit pull. This means you can compare multiple lenders without damaging your score.

Look beyond the monthly payment and focus on the total cost of the loan, including:

- APR

- Origination fees

- Loan term

- Total interest paid

Sometimes a slightly higher monthly payment with a shorter term saves thousands over time.

The Bottom Line

Debt consolidation isn’t about escaping what you owe. It’s about restructuring the payoff process so the math works in your favor.

For borrowers with fair credit in 2026, personal loan rates are still significantly lower than typical credit card rates. That difference alone can shorten repayment timelines and reduce interest costs dramatically.

But the strategy only works when the borrower treats consolidation as a reset point, not a free pass to keep spending.

Use the loan to clear high-interest balances. Keep those cards paid off. Let the installment schedule do its job.

Do that, and the path out of debt becomes a lot clearer.