Commercial Property Insurance Trends in 2026: How Businesses Are Protecting Assets in High-Risk Zones

Commercial property insurance used to be predictable. You budgeted for a modest premium increase each year, renewed the policy, and moved on.

The result? Commercial property insurance rates in 2026 are no longer a simple operational cost. For companies operating in vulnerable regions, coverage itself has become a strategic asset—something that must be earned through risk mitigation and smart planning.

Here’s the uncomfortable reality: the “uninsurable zone” is expanding. Businesses that ignore physical risk exposure may soon find themselves unable to secure coverage at any reasonable price.

That’s not a scare tactic. It’s where the market is headed.

The New Insurance Reality: A Market Splitting in Two

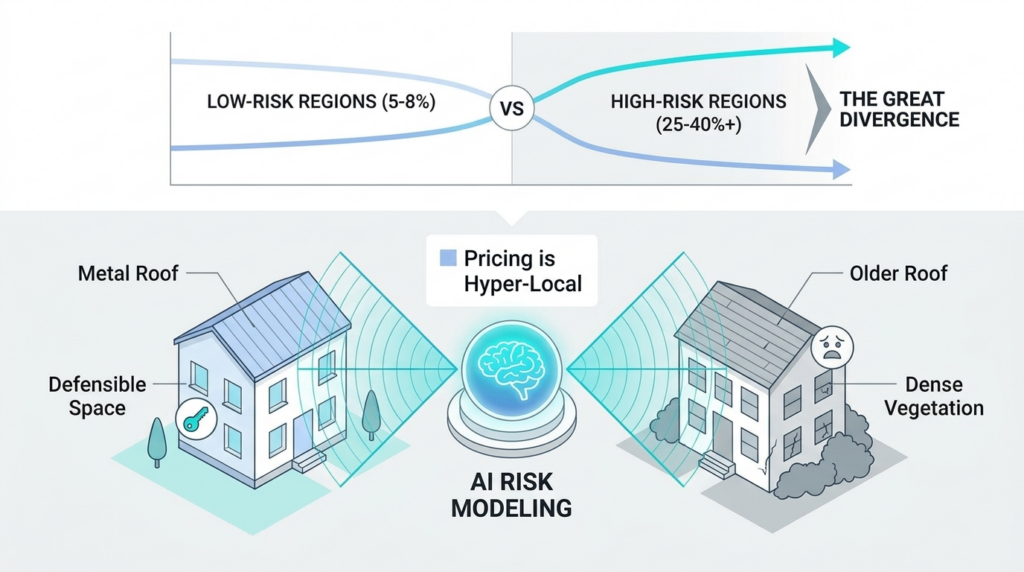

The commercial property insurance market in 2026 is experiencing what many brokers call the Great Divergence.

Low-risk regions are still seeing manageable premium increases. Companies located inland or in stable weather corridors might experience annual adjustments in the 5% to 8% range.

That’s not pleasant, but it’s manageable.

High-risk regions? Entirely different story.

Premium increases in wildfire and hurricane zones are hitting 25% to 40%, sometimes more. In extreme cases, insurers are withdrawing from the market entirely.

The divide between “standard risk” and “distressed risk” properties has widened dramatically.

And here’s the part many property owners miss: this pricing isn’t based only on regional trends anymore.

It’s hyper-local.

How AI Risk Modeling Is Changing Insurance Pricing

Insurance carriers now rely heavily on AI-driven catastrophe modeling.

These systems analyze enormous datasets—weather history, vegetation density, flood elevation maps, storm patterns, building materials, even roof shape.

Then they calculate risk at the parcel level.

Two buildings on the same street may now receive completely different insurance quotes.

Why?

Maybe one property has:

- a metal roof

- elevated electrical systems

- fire-resistant landscaping

- flood barriers installed

The neighboring property might not.

From an underwriting perspective, they’re not equal risks anymore.

This shift means businesses can directly influence their premiums—but only if they actively invest in risk mitigation.

California and Florida: The Front Lines of Insurance Pressure

Certain states illustrate the market shift more clearly than others.

Two stand out.

California’s Wildfire Corridor

California’s wildfire activity over the past decade has fundamentally changed how insurers view exposure in Wildland-Urban Interface (WUI) zones.

Large “mega-fires” have pushed insured losses into the tens of billions. As a result, many carriers have tightened underwriting standards dramatically.

Commercial properties located near fire-prone terrain have seen premium increases averaging 25% to 40% in 2026 alone.

Some carriers now require extensive mitigation evidence before even offering a quote.

Florida’s Hurricane Exposure

Florida faces a different threat: hurricanes and storm surge.

The 2025 hurricane season, one of the most active on record, forced insurers and reinsurers to reevaluate coastal risk models.

Wind damage, storm surge flooding, and infrastructure vulnerability all contribute to higher premiums.

Businesses along the coast now face stricter deductibles, higher windstorm sub-limits, and more complex coverage structures.

In short, insurance is available—but it’s no longer simple.

Why Standard Commercial Policies Are Leaving Dangerous Gaps

Many businesses assume their “all-risk” property policy covers everything.

That assumption can be expensive.

In reality, insurers have quietly tightened policy language over the past several years. Certain high-severity risks—particularly floods and wildfires—are often excluded or severely limited.

That’s where policy endorsements come in.

Without them, businesses in vulnerable areas may discover too late that their most serious risks aren’t actually covered.

Flood Insurance Is No Longer Optional in High-Risk Areas

One of the most common coverage gaps involves flooding.

Standard commercial policies frequently exclude surface water flooding, which is precisely what causes most catastrophic damage during storms.

Given the increasing frequency of flash floods across the Midwest and Northeast, businesses operating in high-risk corridors must explore dedicated flood insurance for business in high-risk zones.

Coverage options typically include:

- private flood insurance carriers

- excess flood markets

- specialized commercial tiers within federal flood programs

Each structure has its own limits and underwriting requirements, but the key takeaway is simple: flood protection must now be addressed separately.

Ignoring it isn’t a strategy.

Parametric Insurance Is Changing the Game

Traditional insurance works through indemnity. After an event occurs, adjusters evaluate damage, calculate losses, and eventually issue payment.

That process can take months.

Businesses waiting for funds during a disaster often struggle to cover immediate expenses—temporary relocation, payroll disruptions, emergency repairs.

That’s why parametric insurance for catastrophes has gained traction in 2026.

Instead of evaluating physical damage, parametric policies trigger payouts when a predefined event occurs.

Examples include:

- a Category 4 hurricane passing through specific coordinates

- wildfire spread reaching a defined radius from a property

- rainfall levels exceeding predetermined thresholds

Once the trigger is met, the payout is automatic.

No lengthy adjustment process.

Funds often arrive within two weeks.

Many companies now combine parametric coverage with traditional property insurance to create a hybrid protection strategy. The parametric payout provides immediate liquidity while the main policy handles structural loss claims.

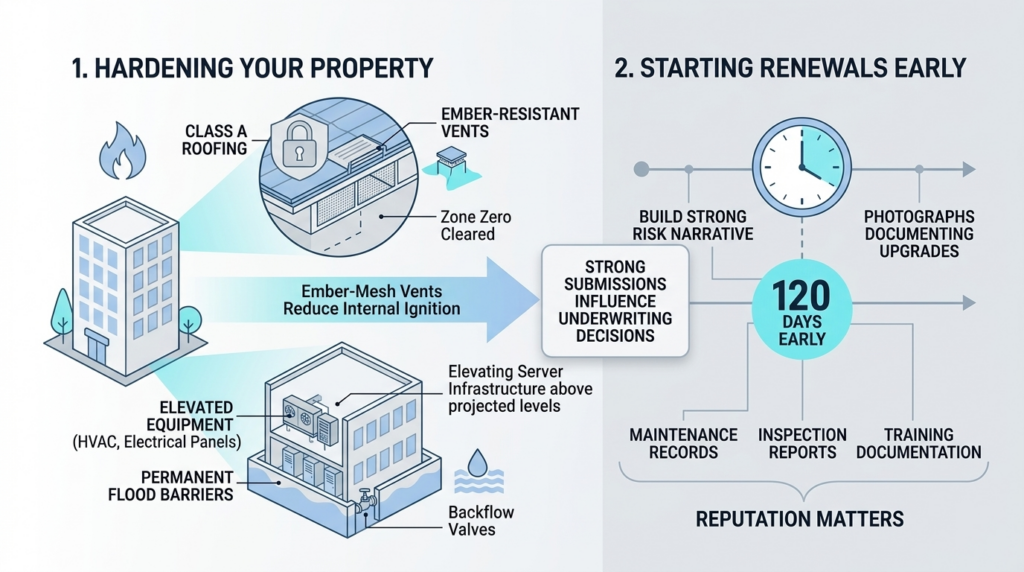

Hardening Your Property: The Only Way to Control Premiums

Insurance carriers are sending a clear message to property owners in 2026: risk mitigation matters.

Businesses that actively improve building resilience are far more likely to secure affordable coverage.

Those that ignore vulnerabilities may face skyrocketing premiums—or policy cancellations.

The good news? Many mitigation steps are straightforward.

Wildfire Protection Strategies for Commercial Properties

Properties located in wildfire zones must demonstrate proactive fire defense.

Common improvements include:

Ember-Resistant Vents

Standard attic vents allow embers to enter during a wildfire. Upgrading to ember-resistant mesh reduces the chance of internal ignition dramatically.

Defensible Space

Creating a vegetation-free buffer around the building—often called Zone Zero—removes combustible materials within five feet of the structure.

Even small changes like replacing wood mulch with gravel can reduce ignition risk.

Class A Roofing Materials

Roofs built with metal, clay tile, or concrete provide far greater resistance to airborne embers than traditional materials.

Insurers increasingly require this upgrade in wildfire-exposed areas.

Flood Resilience Measures Businesses Should Consider

Flood mitigation requires a different set of strategies.

Several improvements significantly strengthen a property’s risk profile.

Permanent Flood Barriers

Integrated flood gates or deployable barriers can protect entry points from rising water levels.

Elevated Equipment

Critical systems such as electrical panels, HVAC units, and server infrastructure should be installed above projected flood levels whenever possible.

Backflow Valves

These valves prevent sewage systems from backing up into buildings during extreme flooding—a surprisingly common source of damage.

Investments like these don’t just reduce physical loss. They signal to insurers that the property owner takes risk management seriously.

That matters during underwriting.

Why Insurance Renewals Now Start 120 Days Early

Renewing commercial insurance used to be a quick process.

Thirty days before expiration, a broker requested quotes and placed coverage.

That timeline is outdated.

Today’s complex insurance placements—especially in high-risk regions—often require layered coverage structures involving multiple carriers. Each insurer accepts a portion of the total exposure.

Building that structure takes time.

That’s why many brokers now follow the 120-day renewal rule.

Start early. Really early.

The Power of a Strong Risk Narrative

When approaching renewal, businesses should provide underwriters with more than just last year’s policy information.

A comprehensive risk narrative can dramatically influence underwriting decisions.

Strong submissions often include:

- photographs documenting mitigation upgrades

- maintenance records for fire suppression systems

- inspection reports for electrical infrastructure

- employee disaster response training documentation

Underwriters aren’t looking for perfect properties. They’re looking for responsible owners who actively reduce risk.

Provide the evidence, and you improve your negotiating position.

Why Proactive Risk Management Is the New Business Strategy

The commercial insurance market isn’t returning to the old normal.

Climate volatility, reinsurance costs, and global catastrophe losses are reshaping underwriting permanently.

Businesses that adapt—by strengthening infrastructure, diversifying coverage, and working closely with experienced brokers—will continue to find coverage.

Those that don’t may struggle.

The equation is straightforward.

Insurance companies are willing to insure well-managed risk. They’re far less interested in unmanaged exposure.

And in a world where extreme weather is becoming more common, that distinction matters more than ever.

Protecting your property isn’t just about rebuilding after disaster.

It’s about staying insurable in the first place.